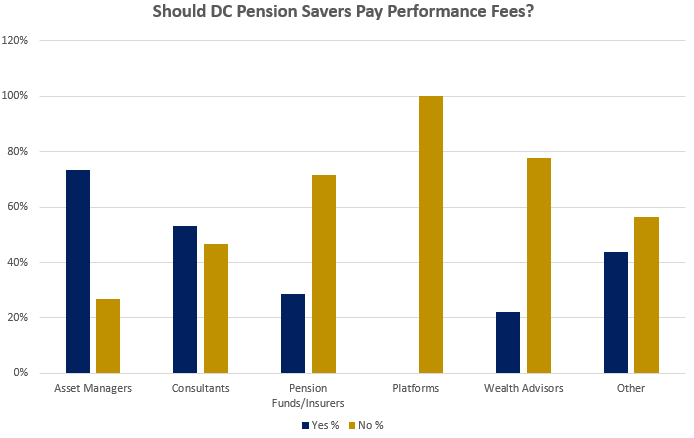

We recently conducted a poll on LinkedIn surveying whether DC savers should pay performance fees. The outcome was very close with 53% of participants saying yes and 47% saying no (114 votes in total). It appears that the tight result masks an interesting (albeit intuitive) underlying dynamic. There is a clear difference between the allocators (Pension Funds, Insurers, Wealth Advisors) and the Asset Managers. The results for Investment Consultants and Other (including Banks, Media and Recruiters) are much more balanced. The results are profiled below:

For illustrative Purpose Only. Source: LinkedIn

We must caveat the analysis in that our sample size is not large enough to claim statistical significance (particularly in the Platform category where we just had a few votes). It appears (shock, horror) we have a case of the Agency Problem on our hands. The Asset Managers may well be feeling that ‘those DC pension schemes don’t know what’s good for them. Performance fees would improve alignment, broaden the opportunity set and improve outcomes’. On the other hand, the pension schemes likely feel that ‘this is just going to increase complexity and cost, which is the opposite of what savers need’.

Inter-temporal fairness – Potential Con

The nature of DC creates a particular issue relating to inter-temporal fairness. In DB schemes, members have a benefit promise which is down to the sponsor to meet. In DC, the retirement outcome for a member depends directly on the performance of their assets. So, different members paying different fees for the same investment is a challenge. Perhaps this is a question of materiality.

We are big believers in DC being a crucial cog in the machine that ‘brings saving to the masses’. As such, the protection that the charge cap has brought for the previously over-charged members generally invested through some of the legacy contract-based arrangements, should be savoured in our view.