Introduction

While in the first half of 2021 price increases were concentrated among relatively few items within the CPI basket, like energy or car prices, price increases have become much more widespread recently. Notably, goods and services inflationary pressures are manifesting themselves alongside nominal wage increases.

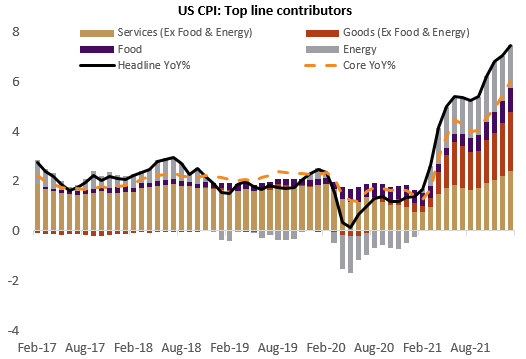

Once again, US consumer price inflation accelerated to a new high since 1982. In January, US Consumer Price Index (CPI) inflation reached 7.5% year-on-year (YoY), with core inflation (excluding food and energy) accelerating to 6.0% YoY. While in the first half of 2021 price increases were concentrated among relatively few items within the CPI basket, like energy or car prices, price increases have become much more widespread recently.

Price increases have been broad based in the US, with all components posting significant increases.

Source: Bloomberg LLP, Fulcrum Asset Management LLP

Source: Cleveland Federal Reserve

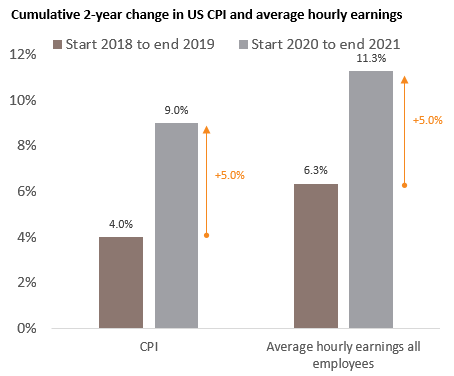

Notably, goods and services inflationary pressures are manifesting themselves alongside nominal wage increases. In the 2-year period from January 2020 to January 2022 the CPI index has increased by a cumulated 9.0%, accelerating by 5 percentage points from a cumulated 4.0% increase in the previous 2-year period from January 2018 to January 2020. With a striking similarity, average hourly earnings have increased by a cumulated 11.3% in the 2-year period from January 2020 to January 2022, also accelerating by 5 percentage points from a 6.3% cumulated increase in the previous 2-year period from January 2018 to January 2020. It looks like a price-wage spiral is happening already.

Source: Bloomberg LLP, Fulcrum Asset Management LLP

With expansionary policies – very sizable government budget deficits largely financed by printing money – but still hesitant aggregate supply of both goods and labour, we do not find it too surprising that consumer prices and wages are moving together, feeding on each other. Buoyant demand for goods and services leads to a combination of higher consumer prices, higher demand for labour, higher employment, and higher nominal wages. In turn, higher employment and wages lead to higher incomes and therefore higher demand for goods and services. And higher wages lead firms to increase prices. At the same time, as current prices are rising, expectations for further price increases gather speed among firms and workers, thereby pushing up prices and wages even more.

This material is for your information only and is not intended to be used by anyone other than you. It is directed at professional clients and eligible counterparties only and is not intended for retail clients. The information contained herein should not be regarded as an offer to sell or as a solicitation of an offer to buy any financial products, including an interest in a fund, or an official confirmation of any transaction. Any such offer or solicitation will be made to qualified investors only by means of an offering memorandum and related subscription agreement. The material is intended only to facilitate your discussions with Fulcrum Asset Management as to the opportunities available to our clients. The given material is subject to change and, although based upon information which we consider reliable, it is not guaranteed as to accuracy or completeness and it should not be relied upon as such. The material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon client’s investment objectives. Funds managed by Fulcrum Asset Management LLP are in general managed using quantitative models though, where this is the case, Fulcrum Asset Management LLP can and do make discretionary decisions on a frequent basis and reserves the right to do so at any point. Past performance is not a guide to future performance. Future returns are not guaranteed and a loss of principal may occur. Fulcrum Asset Management LLP is authorised and regulated by the Financial Conduct Authority of the United Kingdom (No: 230683) and incorporated as a Limited Liability Partnership in England and Wales (No: OC306401) with its registered office at Marble Arch House, 66 Seymour Street, London, W1H 5BT. Fulcrum Asset Management LP is a wholly owned subsidiary of Fulcrum Asset Management LLP incorporated in the State of Delaware, operating from 350 Park Avenue, 13th Floor New York, NY 10022.

©2022 Fulcrum Asset Management LLP. All rights reserved

FC043W 150222

About the Author

Filippo Cartiglia

Filippo is a member of the Investment Team. Before joining Fulcrum in 2020, he was the chief economist at Arrowgrass Capital Partners LLP. Prior to this, Filippo was Managing Director at Goldman Sachs, partner at Newman Ragazzi LLP, and an economist at the International Monetary Fund in Washington. Filippo graduated from Bocconi University in Milan in 1988 and gained a PhD in Economics from Columbia University in New York in 1992.

About the Author

Rahil Ram

Rahil Ram is a Director at Fulcrum Asset Management and is involved in portfolio strategy, portfolio implementation, research, sustainability and idea generation for the discretionary macro and thematic strategies. Prior to joining Fulcrum, Rahil was a strategist within the Asset Allocation team at Legal & General Investment Management for five years, during which time he completed his Masters’ in Actuarial Management from Cass Business School and qualified as an Actuary in 2017.