Introduction

What is the cost of ‘turning down the heat’ in a portfolio? We illustrate how investors can leverage free-to-use climate optimiser tools to understand both trade-offs and opportunities for action

Trade-offs lie at the heart of investing; the preference of more risk-averse investors for the stability of bonds relative to more volatile, but potentially more profitable equities is one classic example. Yet there are no guarantees – as ever, much will depend on investment beliefs.

Investment beliefs also play a key role in the context of climate-aligned and impact investing. For some, applying any climate-related restrictions to the investment universe will necessarily lead to suboptimal capital allocation, as shunned stocks compensate new investors through higher returns. For others, companies lagging on sustainability may be at risk of obsolescence, as changes in technology, regulation and consumer preferences contribute to permanently depress their cash flows – so restrictions can serve as downside protection.

The reality, as always, is nuanced. Investors ‘restricting’ themselves to the tech sector would have generated oversized returns over the past decade; whilst those avoiding energy may have missed out on the oil and gas price rally of recent months.

Rather than search for a single, definitive answer, the ESG for Investors platform equips investors with tools to explore a variety of scenarios and stress-test their beliefs. It provides a big-picture view of the trade-offs investors face when thinking beyond the risk-return framework.

The Climate Optimiser leverages academic research and investment expertise to capture the trade-offs between risk, return and climate impact (measured as the implied temperature rise of a portfolio). Simply put – what is the cost of ‘turning down the heat’ in my portfolio?

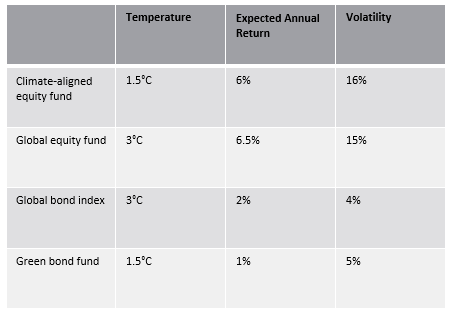

Let us start with a conservative assumption – the existence of a ‘greenium’, whereby climate-aligned equity and bond funds have lower returns and higher volatility than their ‘standard’ counterparts.

Source: Fulcrum Asset Management LLP, Bloomberg, Trucost. We have assumed that broad market indices are aligned with the circa 3°C of global warming implied by the window of uncertainty around current government policies, and modelled historical correlation between representative funds.

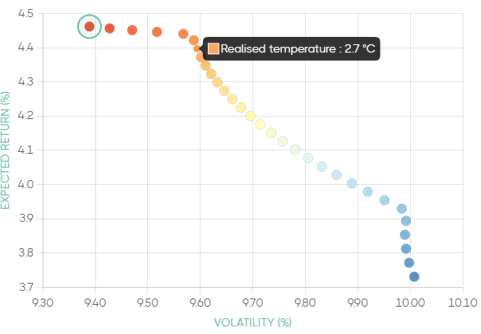

Source: ESG for Investors, Fulcrum Asset Management LLP

Investors can thus begin to build their climate allocation upon such ‘low-regret’ areas. But they may wish to go further. In a previous post, we have argued that markets are already starting to reward companies taking action to address their emissions and working to provide low-carbon solutions.

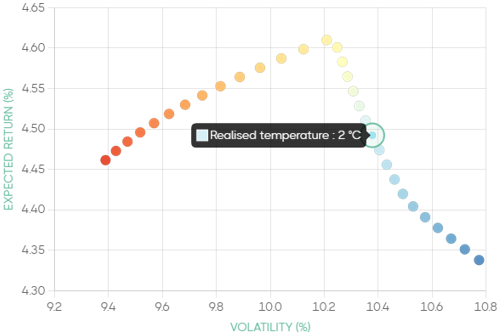

One might thus believe that reducing the implied temperature can help position a portfolio for future upside – or at the very least, not require a sacrifice in return. A slight change in this one assumption – bringing the expected annual return of the climate-aligned equity fund in line with the 6.5% assumed for the global equity index fund, keeping all else equal – leads to a wholly different opportunity set. Here, temperature alignment is actually a driver, rather than a detractor of return, at least up to the point of meeting the upper temperature target (2°C) of the Paris Agreement.

Source: ESG for Investors, Fulcrum Asset Management LLP

Yet it is precisely under uncertainty that the need grows for tools to navigate the transition. We believe the Climate Optimiser can help investors demonstrate to regulators and their beneficiaries how they are considering climate change mitigation as part of their investment process and strategic asset allocation.

As with all optimisers, the tool is sensitive to the assumptions used, but instead of focusing on the micro (assumptions), we believe that the tool highlights the macro, bringing climate change at the heart of portfolio construction.

Modelled, performance results may be used and have certain inherent limitations. Simulated results do not represent actual trading, and thus may not reflect material economic and market factors, such as liquidity constraints, that may have had an impact on actual decision-making. Simulated results are also achieved through retroactive application of a model designed with the benefit of hindsight. No representation is being made that any client will or is likely to achieve results similar to those shown.

This material is for your information only and is not intended to be used by anyone other than you. It is directed at professional clients and eligible counterparties only and is not intended for retail clients. The information contained herein should not be regarded as an offer to sell or as a solicitation of an offer to buy any financial products, including an interest in a fund, or an official confirmation of any transaction. Any such offer or solicitation will be made to qualified investors only by means of an offering memorandum and related subscription agreement. The material is intended only to facilitate your discussions with Fulcrum Asset Management as to the opportunities available to our clients. The given material is subject to change and, although based upon information which we consider reliable, it is not guaranteed as to accuracy or completeness and it should not be relied upon as such. The material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon client’s investment objectives. Funds managed by Fulcrum Asset Management LLP are in general managed using quantitative models though, where this is the case, Fulcrum Asset Management LLP can and do make discretionary decisions on a frequent basis and reserves the right to do so at any point. Past performance is not a guide to future performance. Future returns are not guaranteed and a loss of principal may occur. Fulcrum Asset Management LLP is authorised and regulated by the Financial Conduct Authority of the United Kingdom (No: 230683) and incorporated as a Limited Liability Partnership in England and Wales (No: OC306401) with its registered office at Marble Arch House, 66 Seymour Street, London, W1H 5BT. Fulcrum Asset Management LP is a wholly owned subsidiary of Fulcrum Asset Management LLP incorporated in the State of Delaware, operating from 350 Park Avenue, 13th Floor New York, NY 10022.

©2022 Fulcrum Asset Management LLP. All rights reserved

FC044W 170222

About the Author

Rahil Ram

Rahil Ram is a Director at Fulcrum Asset Management and is involved in portfolio strategy, portfolio implementation, research, sustainability and idea generation for the discretionary macro and thematic strategies. Prior to joining Fulcrum, Rahil was a strategist within the Asset Allocation team at Legal & General Investment Management for five years, during which time he completed his Masters’ in Actuarial Management from Cass Business School and qualified as an Actuary in 2017.

About the Author

Iancu Daramus