The month of March saw a continuation of recent trends, with a further improvement in market sentiment alongside an acceleration in global economic activity. US inflation generally saw upside surprises throughout the month, coinciding with strong data on household consumption, private investment, and business confidence. At the March meeting of the Federal Open Market Committee, officials upgraded their end-2024 projections for GDP growth and core inflation. The median ‘dot’ for the end-2024 Fed Funds Rate remained consistent with three 25bps cuts this year, though the overall distribution of projections shifted higher. Chair Powell and other officials maintained a generally dovish tone, but expressed some concern at recent inflation readings and emphasised that strong growth gives space to delay cuts if necessary. In Europe, policymakers faced a more benign inflation outlook alongside substantially weaker economic activity, leading European Central Bank officials to talk of “swiftly” reducing interest rates. Similarly, at its March meeting, two previously hawkish members of the Bank of England’s Monetary Policy Committee adopted a more accommodative stance.

Meanwhile, in line with expectations, officials at the Bank of Japan raised overnight rates from -0.1% to 0%, ending 8-years of negative interest rates. Furthermore, after months of weak growth, China saw signs of a rebound in economic activity, with industrial output, manufacturing sentiment and exports surprising to the upside.

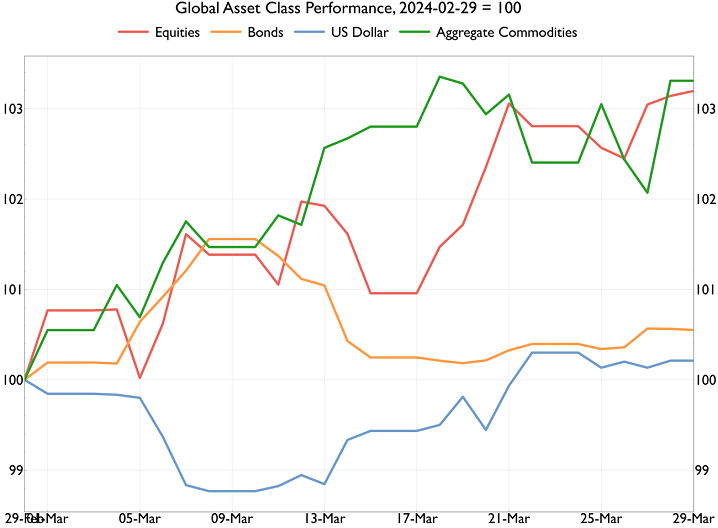

Against this backdrop, global equities were up by +3.2%1 over the month and bonds saw a +0.6%2 increase. The continued divergence in US economic activity and market interest rates helped push the dollar up by +0.2%3. Amidst the general improvement in global growth sentiment, commodities rose by +3.3%4, with increases spread broadly across energy, metals, and agricultural goods. Precious metals experienced a particularly large return of +8.6%5.

Source: Bloomberg