As at 21 March 2024

Author: Gavyn Davies, Executive Chairman

The note below represents my instant view of the Fed’s decisions and guidance yesterday, as distributed to the Fulcrum Investment Committee this morning.

As the markets have noted, the main message from the Federal Open Market Committee (FOMC) yesterday was that a soft landing remains their most likely scenario, and they are working hard to achieve it. By a single vote, the Committee maintained the 3-cut projection for policy rates at the year end, while raising the 2024 Gross Domestic Product (GDP) growth forecast by 0.7% and the core Personal Consumption Expenditures (PCE) inflation forecast by 0.2%. Powell was emphatically on the fence about the timing of the first rate cut, and the market (rightly) interpreted this to imply that he wants to keep a June cut on the agenda.

The only major surprise yesterday, compared to what I had expected, was the important fact that the dots showed a majority of 10-9 votes in favour of 3 cuts or more this year. I assume Waller was the swing voter, deciding to stick with Powell this time. However, it is worth noting that the zeitgeist towards higher dots did occur yesterday and the Committee needs to change its thinking quite significantly in order for a consensus to favour a June cut. We are not there yet.

All that is fairly obvious. Beneath the surface, I would make the following points on both sides of the debate:

On the dovish side

- Powell chose not to emphasise the concerns raised by the latest two inflation prints, and (as expected) described them several times as “bumps in the road”.

- He provided an estimate for core PCE in February of 0.3%, which is similar to the Goldman Sachs (GS) and Morgan Stanley (MS) forecasts, and a bit below our model. He said this was better than last month.

- He mentioned the “alibis” for bad inflation data, including seasonal effects and forthcoming Owners’ Equivalent Rent (OER) disinflation.

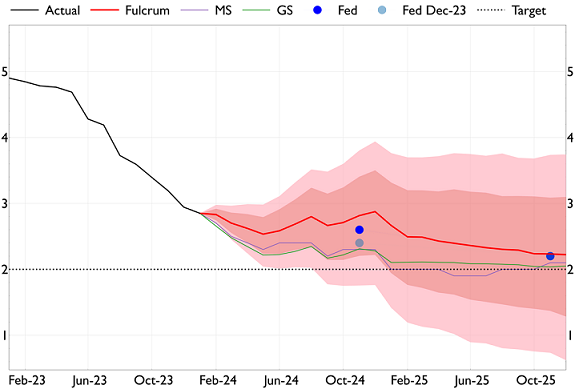

- The end year core PCE inflation forecast was revised up by “only” 0.2%, roughly in between the optimistic GS/MS forecast, and our own less optimistic projection (Graph 1).

Graph 1: Fulcrum Core PCE (YoY %) Forecast

Source: Fulcrum Asset Management, Morgan Stanley, Goldman Sachs

- His implied take on immigration was definitely on the same side that our economics group has been emphasising – i.e., he implied higher immigration does not raise r* or policy rates.

- He seems to have a clear bias concerning the impact of growth surprises on policy rates. Higher GDP growth will be welcomed. Lower growth and an “unexpected” increase in unemployment will lead rapidly to rate cuts. This bias will inevitably impact market pricing considerably going forward.

- He showed no concern whatsoever about the easing in the Financial Conditions Indices (FCIs).

- The longer run dot rose by only 0.1%, much less than expected.

On the hawkish side

- Although the median policy dot remained at 3 cuts this year, it rose by 0.25% in both 2025 and 2026.

- The mean policy rate dot for end-2024 rose from 4.7% to 4.81%. implying only two cuts.

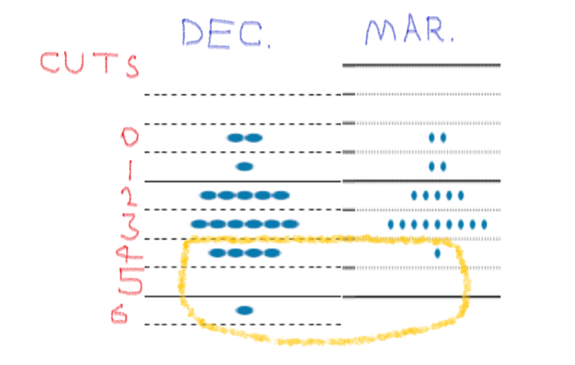

- There was a general rise in the spread of the dots, as shown in John Authers’ entertaining graph below (Graph 2).

Graph 2: John Authers doesn’t use AI

Source: John Authers

- Powell said clearly that the last two inflation prints had not increased anyone’s confidence about the inflation objective and that the FOMC would not ignore news it does not like.

- In the past, Powell has said that “more good news” would be needed to cut rates, not “better news”. This time, there was no mention of the second part of his previous guidance, and it seems clear that the news does need to improve compared with the last two inflation prints.

- Powell followed Kashkari in suggesting that, in the absence of improved news on inflation, the FOMC has the luxury of simply waiting longer to cut rates, unless the economy weakens.

- Powell clearly stated that there is no such weakening in the data right now. It would be “unexpected”.

Conclusion

The main conclusion is that risk assets seem safe (for now) from a sudden lurch towards a “no landing” policy shift by the Fed. However, it is fairly clear from the above points that the Committee (as opposed to Powell himself) is firmly on the fence about a June cut. Although the bias on economic activity is dovish, and the approaching election (in my opinion) points to them starting in June, they do now need two improved inflation prints to permit a June cut.

Our inflation forecasts suggest this outcome is unlikely. Other independent forecasts are more optimistic. The FOMC seems to be in between but still needs to be convinced about the dovish case.