Introduction

It is clear that the Federal Reserve has been surprised by the inflation surge and its persistence. In our view this means that the Fed will not feel constrained by their own past behaviour and instead policy will be informed by the incoming data.

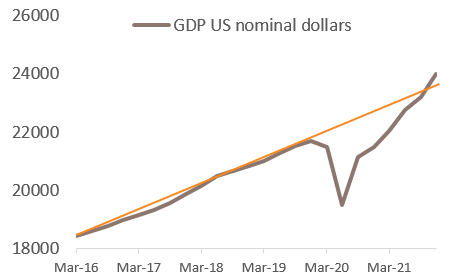

The US economy continues to grow very strongly as evidenced by the latest quarterly nominal GDP numbers. In Q4 2021, US nominal GDP was up by 3.4 per cent quarter-on-quarter (QoQ) non-annualised, 13.6 per cent QoQ annualised, with both real output and the price deflator up by 6.9 per cent QoQ annualised respectively.

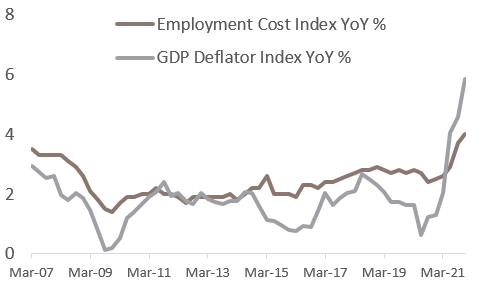

Growth is booming, spurred by the post-pandemic reopening and very large fiscal and monetary stimulus. Nominal GDP had already reached the pre-pandemic level in Q1 2021 and has now also clearly exceeded the pre pandemic trend. Concurrently, inflation indicators have surged, with the GDP deflator which is the broadest indicator of goods and services prices up by 5.9 per cent year-on-year (YoY) and the Employment Cost Index which is a very comprehensive measure of wage inflation up by 4 per cent YoY.

Source: Fulcrum Asset Management LLP, Bloomberg LLP

The rude health of the US economy as evidenced by the data has led the Federal Reserve to announce that they will end quantitative easing (QE) purchases and increase interest rates in March of this year. This was widely expected, but what was more surprising was the shift in language used to communicate the shifting stance of the Fed. Chairman Powell said that going forward the Fed will be “humble and nimble, led by the data”.

It is clear that the Federal Reserve has been surprised by the inflation surge and its persistence. In December 2020, the members of the Federal Open Market Committee (FOMC) expected that the Core PCE deflator would increase by 1.7 per cent in the year from Q4 2020 to Q4 2021. However, it so happened that inflation rose by 4.6 per cent as supply bottlenecks proved more disruptive, demand stronger and labour force participation lower.

A rise of 4.6 per cent is twice as much as both the Fed forecasted and its 2 per cent inflation target. Reflecting this very large miss, Chairman Powell vowed that they will be “humble”, implicitly pledging to rely less on their own forecast and models and more on actual data in formulating policy.

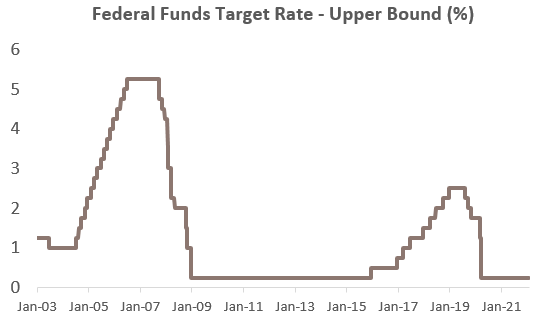

In the meantime, market analysts had speculated that the last two hiking cycles (2004-2006 and 2015-2018) could be seen as a template for the coming years. To put things in perspective, during the 2004-2006 hiking cycle, interest raises were never larger than 25 basis points while during the 2015-2018 cycle, hikes never occurred more frequently than once a quarter and were never larger than 25 basis points.

Source: Fulcrum Asset Management LLP, Bloomberg LLP

However, this time around, Chairman Powell seems to have thrown the towel regarding forward guidance, instead pledging to be “nimble” and emphasising that the Fed now faces very different circumstances to earlier hiking cycles. In our view this means that the Fed will not feel constrained by their own past behaviour and instead policy will be informed by the incoming data. While central bank communication usually tries to take a scientific form, it looks to us that the Fed is increasingly having recourse to art.

This material is for your information only and is not intended to be used by anyone other than you. It is directed at professional clients and eligible counterparties only and is not intended for retail clients. The information contained herein should not be regarded as an offer to sell or as a solicitation of an offer to buy any financial products, including an interest in a fund, or an official confirmation of any transaction. Any such offer or solicitation will be made to qualified investors only by means of an offering memorandum and related subscription agreement. The material is intended only to facilitate your discussions with Fulcrum Asset Management as to the opportunities available to our clients. The given material is subject to change and, although based upon information which we consider reliable, it is not guaranteed as to accuracy or completeness and it should not be relied upon as such. The material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon client’s investment objectives. Funds managed by Fulcrum Asset Management LLP are in general managed using quantitative models though, where this is the case, Fulcrum Asset Management LLP can and do make discretionary decisions on a frequent basis and reserves the right to do so at any point. Past performance is not a guide to future performance. Future returns are not guaranteed and a loss of principal may occur. Fulcrum Asset Management LLP is authorised and regulated by the Financial Conduct Authority of the United Kingdom (No: 230683) and incorporated as a Limited Liability Partnership in England and Wales (No: OC306401) with its registered office at Marble Arch House, 66 Seymour Street, London, W1H 5BT. Fulcrum Asset Management LP is a wholly owned subsidiary of Fulcrum Asset Management LLP incorporated in the State of Delaware, operating from 350 Park Avenue, 13th Floor New York, NY 10022.

©2022 Fulcrum Asset Management LLP. All rights reserved

FC038W 010222

About the Author

Filippo Cartiglia

Filippo is a member of the Investment Team. Before joining Fulcrum in 2020, he was the chief economist at Arrowgrass Capital Partners LLP. Prior to this, Filippo was Managing Director at Goldman Sachs, partner at Newman Ragazzi LLP, and an economist at the International Monetary Fund in Washington. Filippo graduated from Bocconi University in Milan in 1988 and gained a PhD in Economics from Columbia University in New York in 1992.

About the Author

Rahil Ram

Rahil Ram is a Director at Fulcrum Asset Management and is involved in portfolio strategy, portfolio implementation, research, sustainability and idea generation for the discretionary macro and thematic strategies. Prior to joining Fulcrum, Rahil was a strategist within the Asset Allocation team at Legal & General Investment Management for five years, during which time he completed his Masters’ in Actuarial Management from Cass Business School and qualified as an Actuary in 2017.