14 March 2023

Voting at general meetings is a centuries-old practice, but recent years have seen a sea-change in the breadth of issues investors are asked to opine on. Going beyond procedural problems such as appointing of auditors and the issuance of shares, topics such as ending fossil fuel financing, conducting a ‘racial equity audit’ or quantifying the monetary benefits of diversity initiatives are increasingly present on the ballot. And with contentious meetings that may lead to congressional hearings as well as activist a capella listening, the scrutiny on shareholder behaviour has also increased. In what follows, we share our reflections on the past year and the evolution of our own voting approach.

Scorned proposals?

In 2022, we have continued to encourage companies to step up on sustainability through our votes, by supporting resolutions calling for reduction in emissions or plastic packaging, action on labour standards and human rights, or improved transparency with regards to political lobbying. We illustrate this below, showing Fulcrum’s high levels of support across the universe of shareholder proposals selected by responsible investment NGO ShareAction as the basis of their recently released ‘Voting Matters’ report.

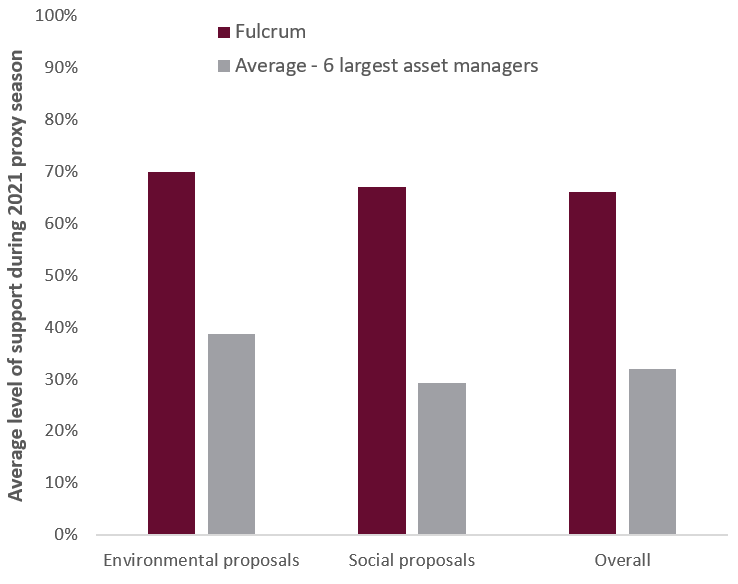

Fulcrum supported more proposals than many of the world’s largest asset managers during the 2020-2021 proxy season…

…and the 2021-2022 proxy season…

Chart data sources: ShareAction (“Voting Matters”, 2021 and 2022 editions), Fulcrum Asset Management, Glass Lewis

Whilst we did not believe in restrictions as a one-size-fits-all rule, there may be individual cases where we would be supportive: we have recently joined forces with investors managing over $1 trillion in assets, calling on French financial giant BNP Paribas to stop the financing of new oil and gas fields. In our view, a cleaner loan portfolio would help improve the bank’s cost of capital, reduce reputational risk and support the company’s stated ambitions to be a leader in sustainable financing.

Direct director aim

2022 was the first full proxy season where the Glass Lewis Climate Policy, chosen as our default set of voting recommendations, was in operation. An important rationale for choosing this policy is to go beyond whatever shareholder resolutions happen to be on the ballot, by codifying certain high-level principles that we would expect all or most companies to meet.

Having independent directors (particularly on key board committees), disclosing your company’s greenhouse gas emissions, ensuring remuneration criteria do not undermine a company’s sustainability objectives – these are some of the requirements that can trigger a voting sanction. By sanctioning a director or their pay, we believe we may sometimes send a stronger signal than merely by supporting shareholder proposals (which are often advisory). Throughout 2022, we have cast:

- 452 votes against directors for insufficient oversight, disclosures and targets in the area of sustainability

- 334 votes against pay for misaligned environmental and/or social incentives; and

- 1000 votes against companies, primarily for principles-based sustainability concerns.

Taking the temperature

Another notable feature of discussions around the past proxy season is increased polarisation. Some critics accuse asset managers of abdicating or abusing their responsibilities (by relying on proxy advisors, instead of doing their own due diligence or allowing full voting control to the end beneficiaries of funds). However, many areas of investing require balancing in-house and external expertise. A fund manager may model the creditworthiness of a particular company in detail, but for a portfolio of hundreds or thousands of names, the opinion of credit ratings agencies is likely to feature more prominently. Similarly in the context of voting, the informational requirements grow exponentially (for some asset managers the resolution tally can range up to hundreds of thousands per proxy season). Proxy voting agencies can help bridge this gap by providing independent analysis and benchmarking of companies, as well as, as already highlighted, a degree of customization.

Far from abdicating responsibility, the Fulcrum Stewardship Committee regularly reviews contentious votes: in 2022, we have overridden the recommendations of our proxy advisor in around a third of the 150 votes discussed, where we believed company-specific circumstances merited additional consideration.

A separate critique is whether encouraging companies to go beyond mere legal compliance in areas such as sustainability means that asset managers are pursuing a ‘political agenda’ divorced from shareholder value. In response, it is worth revisiting arguably the most influential articulation of this idea – Milton Friedman’s famous injunction that ‘The Social Responsibility Of Business Is to Increase Its Profits’ (incidentally, an article partly prompted by sustainability-related shareholder proposals filed in the 1970s). Friedman made an impassioned case for maintaining a focus on shareholder primacy at the expense of more vaguely defined stakeholder or societal goals. Less appreciated, however, is Friedman’s full formulation of the duty of the corporate executive: “to make as much money as possible while conforming to the basic rules of the society, both those embodied in law and those embodied in ethical custom.” (my emphasis). Clearly, when it comes to sustainability, both the law and social expectations are evolving.

In sum, our stewardship efforts aim to encourage progress in the market, but without losing sight of materiality. We will continue to use the tools at our disposal – voting, direct and collective engagement, capital allocation – to pursue this ‘golden middle ground’.