Author: Gavyn Davies, Executive Chairman

Attempting to make sense of this recession right now is like peering though a thick fog. To fully understand its nature, we will need to wait until full data for second-quarter gross domestic product are published in July.

But the downturn’s basic anatomy is starting to become apparent, especially in the US, where the figures appear earlier than elsewhere. In many ways, this is just a much larger version of a normal recession.

One thing that seems different this time is that much of the slump in US consumer spending has been accompanied not by declining personal incomes but by a surge in savings, which suggests consumers may remain cautious during the recovery. US national accounts always estimate real gross domestic product using three complementary methods: value added, expenditures and income flows.

Now that we are halfway through the second quarter, the most reliable way of estimating eventual output growth is to use value added indicators, such as business surveys and industrial production. The Atlanta Federal Reserve Bank’s GDP Now estimates that second-quarter GDP will fall at an annualised rate of 41.9 per cent compared to the first quarter. The New York Fed’s nowcast shows an annualised drop of 30.5 per cent. This would make it the worst quarter for GDP growth since the 1930s.

The nature, though not the scale, of the response in the labour market has been in some ways typical of previous recessions. Unemployment rates may rise by as much as 20 percentage points, according to Federal Reserve Chairman Jay Powell, and hours worked in the private sector have already declined by about 15 per cent between March and April, leaving overall productivity (output per hour worked) broadly unchanged from pre-pandemic levels.

In many recessions, the immediate decline in employment was reflected in a drop in private incomes, since the wages lost by the newly unemployed were not fully replaced by government unemployment benefits. There was therefore a squeeze on real disposable income that caused a slowdown in consumer spending, while the savings ratio changed little.

The recession of 2020 is different, at least so far. Nearly 39m Americans have lost their jobs since the pandemic began, and real disposable income did temporarily decline in the March US data. But that was partly because payments of unemployment insurance benefits were delayed by administrative bottlenecks.

For the second quarter, JPMorgan forecasts that government support from unemployment and the Cares Act, including tax cuts, will restore much of the drop in personal disposable incomeand Goldman Sachs estimates that 75 per cent of the newly unemployed will receive more in government payments than they previously earned in wages. That degree of income replacement would be an impressive step for US public policy, as Paul Krugman argues.

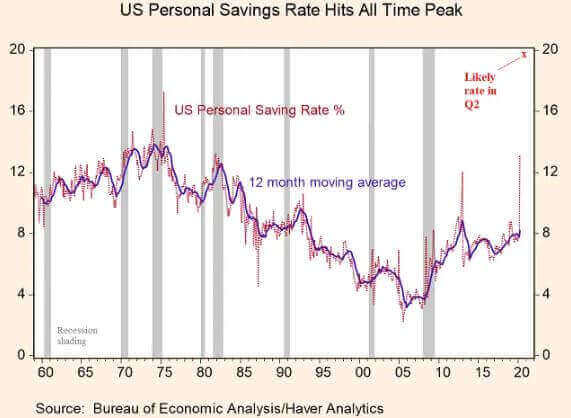

Despite this income support, consumer spending has collapsed, especially in service sectors and on discretionary goods such as autos. As a result, the savings ratio could well rise to about 20 per cent of household income.

The key question for the economic recovery is how much of this increase will be reversed as the lockdowns are eased. Part of the decline in spending has been involuntary and will be restored as restaurants and stores reopen and work patterns return to normal. But the decline in discretionary spending on big-ticket and other items may last longer, especially if the emergency rise in unemployment benefits ends after the end of July, as planned.

The direct US fiscal stimulus in response to the virus has been about 13 per cent of GDP, and this has maintained household incomes as unemployment has soared. Nevertheless, households have curtailed spending causing a recession. Any withdrawal of the fiscal stimulus, at a time when precautionary savings remain high, could continue to depress spending and prolong the recession.

The US is far from alone among the major economies in facing this dilemma. The collapse in UK retail sales relative to household income shown in the latest data suggests that savings have rocketed as consumers have become pessimistic. Chancellor Rishi Sunak’s decisions on how to withdraw wage support as he winds down the furlough scheme are looking more difficult than ever.

US household savings rate may be at all time highs in current quarter

The American household sector has been hit with a huge decline in employment in the second quarter, but the payment of government subsidies and transfers to employers and employees has prevented any meaningful decline in personal disposable income. As a result of these income support measures, and the slump in consumption, the savings rate has rocketed.

Attempting to make sense of this recession right now is like peering though a thick fog. To fully understand its nature, we will need to wait until full data for second-quarter gross domestic product are published in July.