23 September 2022

Amid the current market and geopolitical turmoil, one of the few ‘green’ linings has been the renewed political determination to accelerate the transition to a low-carbon economy and away from fossil fuels. Recent analysis from the International Energy Agency finds that renewables are growing faster than overall power demand in 2022, leading to a projected decline in global power sector CO2 emissions despite rising coal use in Europe; the European Council has agreed strengthened targets for renewables and energy efficiency under its ‘Fit for 55’ package; meanwhile, in the US, President Biden’s Inflation Reduction Act may see over $300 billion allocated to climate measures, including investments in domestic clean energy and tax rebates for consumers, and potentially ending years of political deadlock on this issue. Australia, too, has shown newfound political momentum through the passage of a significant climate change bill in early September. India has revised upwards its targets for clean energy, whilst China continues large-scale cleantech capital deployment, with its investments in solar and wind up 173% and 107% year-on-year.

These are some of the developments that strengthen our belief, as a macro-focused investment house, in the investment signal coming from the interplay between climate policy and technology, as efforts grow to put the world’s economy and financial system on track towards net zero.

Sources: https://zerotracker.net/analysis/net-zero-stocktake-2022/;

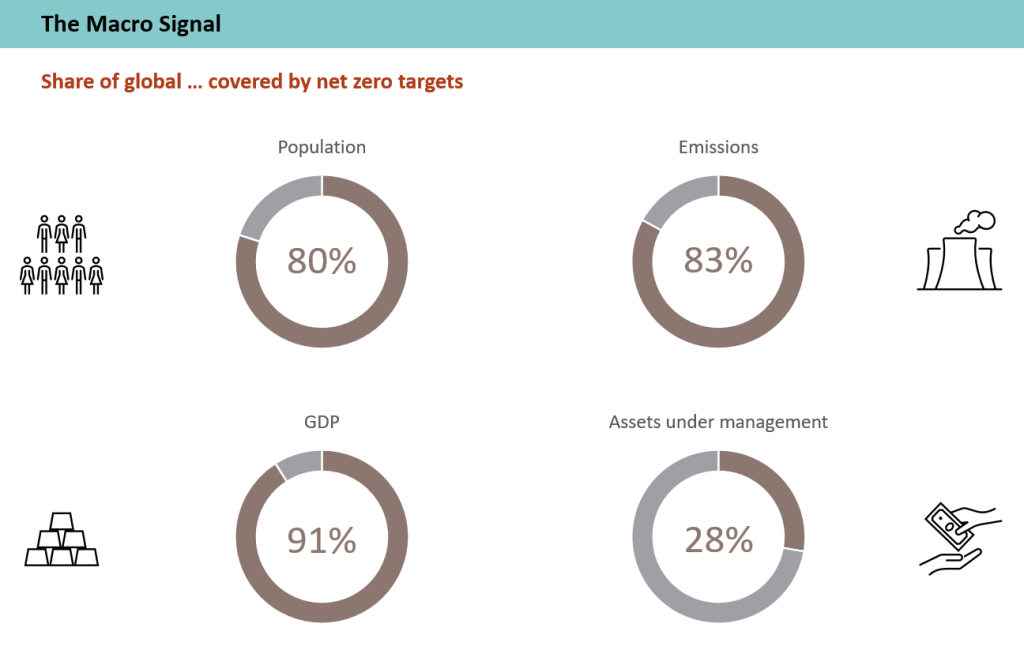

AUM: GFANZ assets under management or advice as % of global financial assets, Dec 2021.

GFANZ, Fulcrum

More than 90% of global GDP has been committed, top-down, by governments, to net zero. And financial institution after institution have rapidly joined the ranks of the Global Financial Alliance for Net Zero (GFANZ) – now covering almost a third of global assets under management or advice.

For sure, the energy transition will not be a linear process, and many uncertainties remain. But the signal is strong enough, in our view, to warrant action today, creating an opportunity for early investors seeking to position their portfolios to anticipate future climate-related repricing of assets.

At Fulcrum, this alignment has already begun, with the launch of our first climate change strategy, and our pledge that, by the end of 2022, the majority of our long-term directional equities will only be invested in companies aligned with the goals of the Paris Agreement.

We are proud of our journey so far, but recognize there is still much to be done. That is why we were honoured to be invited, in early 2022, to join the Portfolio Alignment Measurement workstream in GFANZ, with members of our management board, investment and research teams working on defining and implementing best practice in this area, alongside representatives from leading financial institutions.

Hard questions about a warming planet

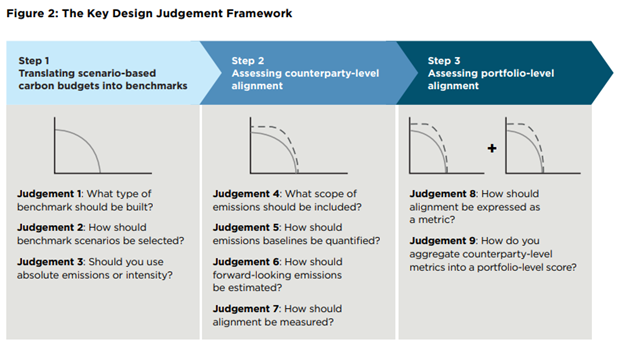

It is absolute greenhouse gas emissions that are driving climate change, but it is relative emissions (e.g. per unit of sales) that give you a measure of which companies are more ‘carbon-efficient’ – so which metric should investors choose? It is past sales that companies report in quarterly earnings, but future cashflows that investors aim to value; similarly, should investors account only for the current and past emissions of companies, or also look at their plans and targets? These are some of the questions that the workstream aimed to tackle, culminating in the publication, last month, of a significant new report with timely practical case studies.

Measuring Portfolio Alignment: Enhancement, Convergence, and Adoption aims to offer guidance on multiple technical aspects, structured around 9 ‘key judgements’.

Source: GFANZ.

As the questions above illustrate, these issues are not without theoretical and practical challenges, and investors may reasonably disagree about the best approach. After all, just as there is no single way to invest, there may not be a single way to align investments, which is uniformly applicable across all asset classes, regions and timelines.

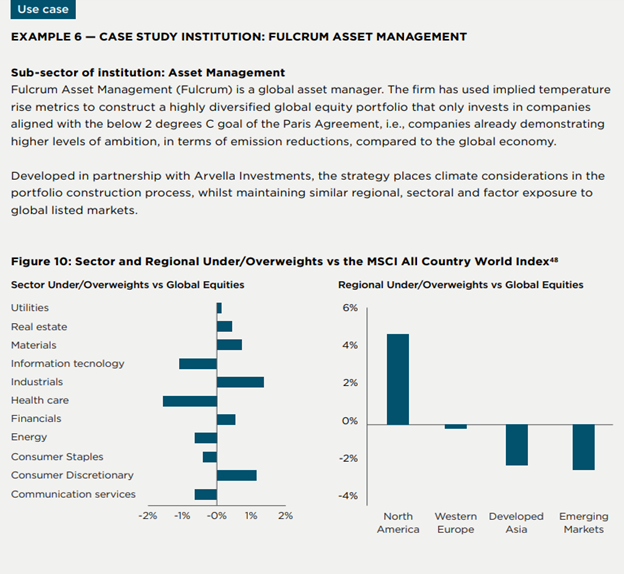

Nonetheless, we believe this report can make an important contribution in bringing the industry closer to convergence (even if complete consensus may ultimately prove elusive). In particular, we wholeheartedly welcome the report’s emphasis on the importance of forward-looking metrics – a stance echoed by the UK government recommending pension trustees adopt such metrics in regular reporting and highlighting alignment measurement as a ‘key’ workstream in GFANZ – and are proud to have our approach to equity portfolio construction featured as a case study in the report.

Sources: MSCI, Bloomberg LLP, S&P Global Trucost and Fulcrum Asset Management (accurate as of 30th June 2022). Image source: GFANZ. For the full case study, see pages 23-24 of the report.

At the same time, there remain many important areas requiring future work, and we aim to support the workstream tackle them over time. Fulcrum have responded to the public consultation that followed the publication of the report, outlining our views on:

- The importance of external target verification (e.g. via the Science Based Targets initiative) as an indicator of credibility

- The benefits of applying alignment constraints at the issuer level, not just for overall portfolio metrics

- The materiality of Scope 3 emissions

- How a thematic approach can supplement emissions metrics in capturing the contribution of climate technologies

Conclusion

We believe the information content of climate-related data far outweighs the methodological challenges, allowing investors to take action and have an impact on climate change today. In an otherwise adversarial market, addressing climate change is one of the few areas that is not a zero-sum game. We look forward to future collaboration, through GFANZ and other industry networks, to help drive further progress in this area.