24 June 2020

Author: Gavyn Davies, Executive Chairman

One of the long-term consequences of the 2008 financial crisis was a lack of safe assets that could be used by institutions to store their wealth, meet regulatory requirements and provide collateral to borrow additional funds.

This problem has been identified as an important reason for low capital investment and the slow growth rate in the global economy in the past decade. It was also a prime cause of the European sovereign debt crisis, which peaked in 2012.

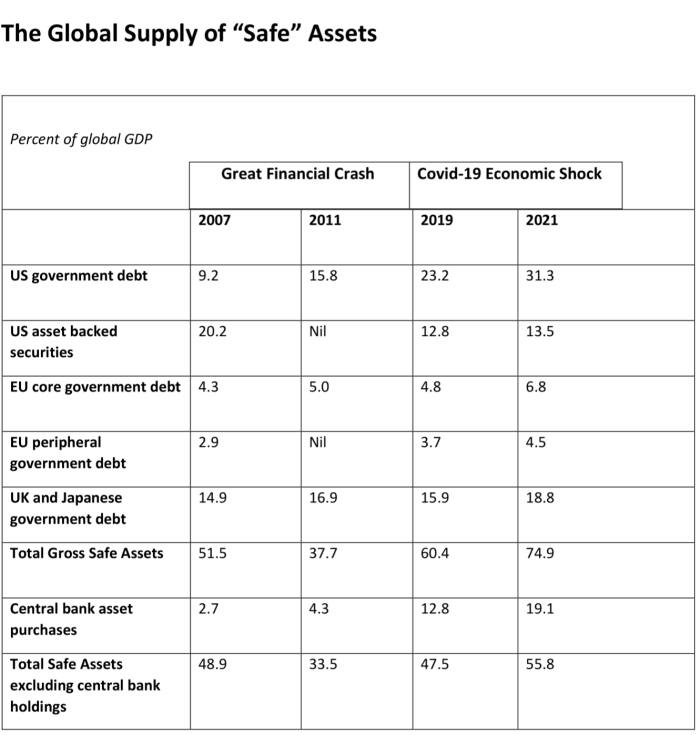

But a silver lining from the Covid-19 shock is that the policy response may actually alleviate the safe-asset shortage, according to new research by Fulcrum economists (see table). That’s because it will leave a legacy of much higher government debt in the most advanced economies, including the US, which is the main global source of these assets.

A safe asset is usually defined as a financial instrument that is unlikely to experience a big increase in default risk, even at the darkest times in the economic cycle. It is therefore a reliable source of liquidity when riskier assets suddenly lose value. It will often face inflation and interest rate risk, but usually not default risk.

Before 2008, the supply of high-grade government bonds in the advanced economies was restricted because budget deficits were declining. To meet demand, the private sector created AAA-rated tranches of mortgage and other credit products. But these products proved to be anything but safe, prompting a stampede into government bonds, especially US treasuries and German bonds, which were deemed immune from default risk. New banking regulations requiring them to increase their capital and liquidity buffers later made this outcome more permanent.

The definitions and assumptions used in this table are explained in full in a research note by Fulcrum economists

Why did this create a serious problem? In theory, since the price of government bonds is determined in a free market, a supply shortage would be expected to be eliminated by higher bond prices and therefore lower yields. This, indeed, happened, and after 2015 the US currency also appreciated, choking off excess demand for dollar-based assets.

The trouble for the world economy arose when bond yields in many economies approached zero, making it all but impossible to achieve the further decline in yields needed to rein in demand for safe assets.

Economists including Ricardo Caballero and Emmanuel Farhi say that in some models this can result in a “safety trap” that affects the global economy. This is a close cousin of the “liquidity trap” that appears in many New Keynesian models.

Because interest rates cannot fall enough to balance the supply and demand for safe assets, national income and wealth shrink to eliminate the excess demand for them.

Messrs Caballero and Farhi, along with Pierre-Olivier Gourinchas, suggest that the flight to safety increases the equity risk premium relative to safe assets, accounting for part of the weakness of capital expenditure in the advanced economies since 2009.

Given the potentially serious consequences of the safety trap, it would be alarming if the Covid-19 shock replicated the financial crisis by making the imbalance even worse — but this seems unlikely to happen. The rise in public debt, and so the supply of safe assets, will this time be both quicker and larger. In addition, the financial system has so far been more insulated from the shock, so it is less likely that the highest rated credit tranches in the US mortgage market will fall out of the category of safe assets.

Direct purchases of corporate credit and loans by the US Federal Reserve may protect the asset-backed securities market from widespread default. In the eurozone, the steps taken towards an EU-backed recovery bond should add to safe assets, instead of wiping them out.

This growing supply of safe assets could, however, be offset by rising demand. Central bank asset-purchase programmes will remove government bonds and the safest tranches of securitised credit products from the hands of the private sector.

In the longer term, the overall effects on bond yields will also be influenced by the impact of the Covid-19 shock on net private savings. According to research by Oxford Economics, which warned about the worrying trend in safe-asset supply just before the pandemic, a possible shift towards excess private savings and reduced investment after this recession could offset the initial improvements in safe-asset supply.

These longer-term effects are very hard to predict. The good news is that the Covid-19 recession will almost certainly increase the supply of safe assets in the immediate future, alleviating the problem as the global economy starts to recover.